John Curtis-Oliver of Boyden UAE makes the case for telecoms sector innovation in the Middle East and Africa.

As Warren Buffet once said, we should “be fearful when others are greedy and greedy when others are fearful”. Since arriving in the region in 2005, I have focused on hiring leaders into the telecoms and technology sectors. I have always been struck by an overriding sense that the leaders of the telco operators seem content to follow the crowd rather than to pave the way. Year after year, the leaders of the major telco groups deliver similar messages to each other with the current message being all aboard the digital bandwagon. Have our telco leaders been guilty of ignoring Mr. Buffet’s advice?

What is the future for the telco sector in our region? I remember in 2006, advising a candidate who was due to be interviewed by one of the major telco groups as the head of the M&A team. To paraphrase his thoughts, he suggested that instead of paying $X billion for the 9th mobile licence in Togo or Yemen (no offense to my dear friends from Togo and Yemen), perhaps he advocated, it might be interesting to build a diverse portfolio of assets investing in ISPs, internet start-ups, ICT, future technologies, IT services, system integrators or anything else we can think of with a view to being able to offer a fully-fledged service to the corporate segment and consumer segments? I told him that he may be ahead of his time. For those of us who are old enough to remember, this was the era of new licence issuing and the proverbial beauty parades. The client felt he did not truly understand the role. When we seek to understand some of the challenges faced by the telco sector now, we can track back to this era. Even in 2006, the operators in the region quietly admitted that, while they had control over the consumer segment from a voice and data perspective, with the corporate sector, they had no choice but to form partnerships in order to offer a full service. Why did they resist rather than drive technological innovation?

LIGHT AT THE END OF THE INNOVATION TUNNEL

During the 2017 Mobile World Congress in Barcelona, there appeared to be great enthusiasm around new technology and the potential for a bright future but an overriding sense of doubt as to which, if any, of the operators in the Middle East and Africa are truly ready to capitalise on the opportunity. Everyone seemed to want to change and transform and innovate, but was this a push to drive performance improvements through innovation or a reluctant admission that the world has changed and the current modus operandi might have a short shelf life?

While talking to some brilliant start-up companies at the 4YFN event, I found that a common complaint was the lack of access to the key decision makers from the telco operators. Even the

start-ups led by ex telco industry executives with direct access to decision makers made this complaint. It seemed ironic that, while the operators’ leadership talk of changing the model,

leading the digital revolution and breaking away from the traditional revenue streams, the short shuttle from the main event to the 4YFN event was a bridge too far. Who knows what hidden gems may have been there?

On behalf of the start-ups, my message to CEOs is this: next year, or next time there is a major industry event, split your delegation into teams, tell them to go into the halls and the 4YFN (or equivalent) start-up event and come back to you with the two to three best companies for you to meet. Give each of them ten minutes of your time and the chance to pitch their solution. If nothing else, it will give the start-ups hope. If the start-ups do not see a light at the end of the tunnel, innovation will die and the industry will go backwards.

Over the past few weeks, I have been surveying senior executives from the telco sector. I surveyed directors, VPs and CXOs from the major telco groups in the MEA region in order to build up a picture of how they view the industry. I have been asked to emphasise that those quoted in this article are giving their own opinions and not necessarily the opinions of their employers.

RATING THE TELCO OPERATORS

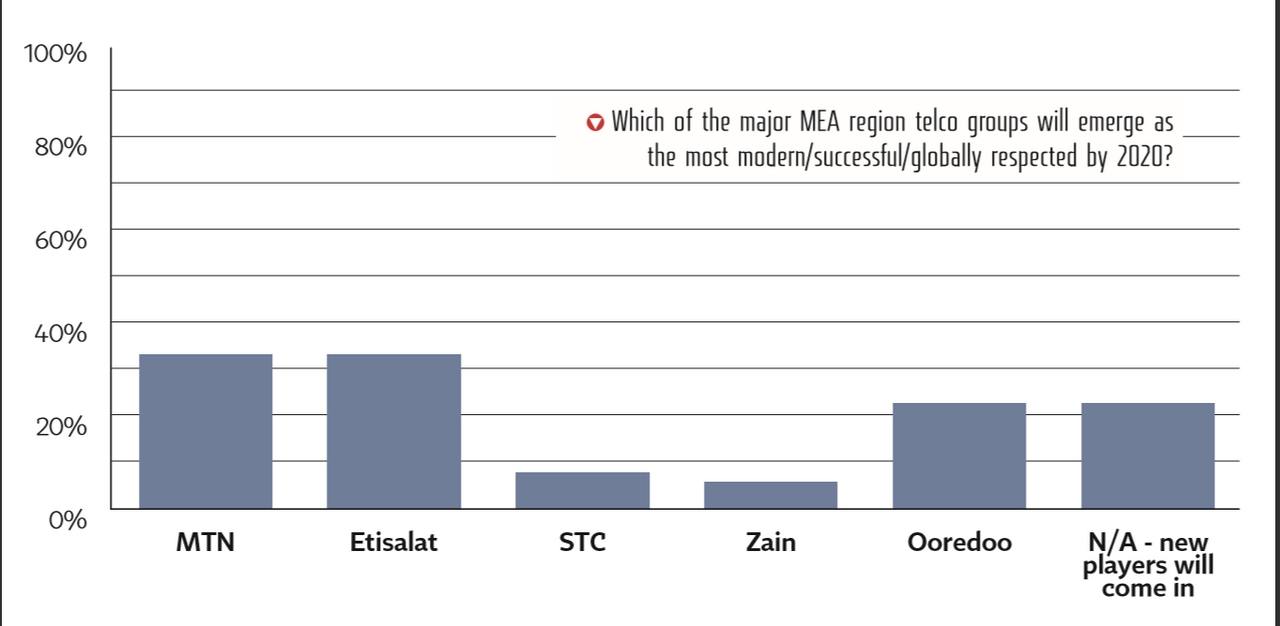

In response to the question “Which of the major MEA region originated telco groups will emerge as the most modern / successful / globally respected by 2020?”, respondents had the option to select more than one. Out of Ooredoo, Zain, STC, Etisalat and MTN, it was Etisalat and MTN who led the way, albeit the margin of their lead over Ooredoo is not significant.

Those voting for MTN felt that, as it is not an incumbent, it may be less bound by political constraints than others and thus relatively more free to grow its business as it sees fit. Etisalat voters pointed to a secure revenue base from the home operations, a strong financial position and the chance to drive innovation initially in a home market with a wealthy and technology hungry customer base, willing to adapt to new innovations. I was surprised that STC did not garner more support. STC appears ready to lead rather than react to technological advancements. It will not get everything right but with an enviable financial foundation and a desire to drive innovation, it could be the one to watch.

The most interesting result was the 22.9% of respondents who chose the response ‘N/A - all of the above will become more localised in their approach and new players will come in.’

Rupesh Sharma, CFO of Ooredoo Kuwait, noted that “operators are too focused on protecting existing revenues and not investing heavily enough in creating new revenue streams.” He, amongst others, felt that this may open the door to new entrants in the near future. These new entrants need not be licensed operators in the traditional sense.

Other respondents, who preferred to remain anonymous, lamented conservatism amongst boards and shareholders. The accusation levelled against them was that they were too focused on short term dividends and quarterly KPIs and were not prepared to build for the future. This conservatism and desire to cling to the past, it would appear, impacts CEO behaviour. There is a sense of just trying to get through the next board meeting with an inevitable survivalist mentality. I was fortunate enough to attend an event hosted by Oracle and to hear a brilliant presentation by their CEO, Mark Hurd. He pointed out that ‘the average CEO tenure is now 18 quarters.’ He went on to state that ‘40% do not last 18 months.’ Planning 5-10 years ahead means reinvesting into the business and a short term reduction in margins so that your successor can earn an enormous bonus five years later. How many of us would sign up for that deal?

INNOVATION OPPORTUNITIES

While considering the attempts of the telco sector to innovate, I asked the question: "Why have telecom operators failed to capitalise on market opportunities leaving most of the innovation to smaller tech companies? The breakdown of responses was as below:

- Inefficient operating models/processes reduce ability to move as quickly as the market (61.3%)

- Historical complacency means the basics are still not fixed. CEOs need to put in the fundamentals before thinking of innovation (42.9%)

- Sources of funding are often government/sovereign. Due to challenges in other sectors, boards are financially nervous and risk averse (26.3%)

- I disagree with the concept in the question - I see extensive innovation and attempts to change the model (6.1%)

- Too many CEOs moving from one group to another within the region or being promoted from within which limits the amount of fresh thinking (4.1%)

- Other (18%)

It is noteworthy to see just how few were satisfied with the attempts of the operators to innovate and change the model. As all of the respondents were from the operator segment, this response is perhaps the most concerning of all.

A recurring theme is the risk averse nature of boards. If we consider the scenario at Mobily, where the challenges are well documented, five years ago the then CEO was vocal about the way a telco should look in the future and many now are making similar statements. However, when a company is forced to go through a root and branch clean up, it inevitably has to focus on survival rather than innovation. Although Mobily is an extreme case, there are many less extreme examples and it is understandable that CEOs will focus on fixing basics to prioritise keeping the business afloat over long term innovation.

One executive, who preferred to remain anonymous noted: “In the end, I see one infrastructure being built by maybe two operators and then many companies innovating utilising the infrastructure”. It is certainly true that as we move up the Gs there will be more than enough capacity in the pipe, regardless as to whether this pipe is virtual or physical in the future.The value will be entirely in the services.

Andrew White, former chief strategy officer at Zain KSA notes that the telco sector “offers an essential service. That service is connectivity. The industry needs to structure itself to deliver utility style returns: high capital employed, relatively low return, low risk.” The inability to capitalise on the digital revolution he felt is “because the business model is fundamentally different. Silicon Valley style: low investment, very high risk, human capital very important. Telco style: high investment, conservative approach, limited value on human capital”.

Those who are in protected markets with reliable income streams have less need to drive innovation but are financially better placed to make the investment. Those who are in saturated and highly competitive markets need to innovate to stay ahead but may not be financially positioned to make the necessary investments.

INNOVATION IS A CURIOUS BEAST

A senior executive with one of the major incumbent telco groups, who preferred to remain anonymous, disagreed with the naysayers and, referring to STC, Etisalat, Ooredoo, Zain and MTN, noted: “I believe all of the above have the chance to change their business models and be successful in the markets they operate. All of above are ‘talking the talk’ and the challenge now is to ‘walk the walk’ and evolve their businesses to transform to become leading digital players in this rapidly changing global market. By digital, I not only mean digital services such as cloud, IOT or M2M but also the way we utilise technologies and build new processes to transform the way we interact with customers and provide the best customer experience.”

In today’s world CEOs need to be chief digital officers. The whole business needs to be digitalised. Making better use of customer and other data with a view to driving operational improvements to support their needs is key and has far heavier short term impact than the more left field initiatives. For years there have been concerns about innovation for innovation’s sake: ‘Companies innovate faster than customers’ lives change…. What people are looking to get done remains remarkably consistent, but products always improve.’ (Christensen & Roth 2004)

Is true innovation a simple phone which never drops a call and a battery which lasts for several days? Do we really need a connected car? Indeed, while the more creative uses of technologies are to be applauded, there is a risk in the more traditional telcos that the digital business operates outside of the main system and delivers only a fraction of its potential value.

TELCO OF THE FUTURE

Despite the challenges the market faces and the relative lack of innovation, 73.5% suggested that the future of the telco in the region will be a multi-service player offering a range of consultancy, technology, digital, managed services and other solutions competing against SIs and IT services companies, while creating new and innovative solutions. For innovation to happen,people need to be free to think and take risks.

If telcos are really utilities, should we not compare them to the electricity and water companies? Be a pipe but be the best pipe you possibly can! Perhaps the way forward is to partner with or invest in companies better placed to innovate and accept that the operators will provide the connectivity. While the majority of CEOs proclaim the need to lead the digital revolution, will we see a brave CEO who happily transforms his company into a utility or connectivity provider and does it with pride? Perhaps it is time to be fearful while others are greedy?

Ahmed Abdel Latif, group chief wholesale officer of Batelco noted that: “Telcos are torn between increasing investment requirements on the network side and declining per-user/

per-service revenue on the sales side. The future will see upstream players (the 4G/5G network builders, spectrum licence holders, tower operators, and broadband network developers) providing “connectivity/transport” services to downstream players who focus on providing specific services (private networks, home automation, managed security, content/ entertainment, e-health, and m-banking) to a segment or more (consumer, enterprise, SME, MNC, and government). Success comes from focus on delivering a specific capability/utility to customers, rather than trying to be everything to everyone. The future telco is not a single monolithic entity, but rather several specialist organisms within a more complex ecosystem. This upstream/downstream view may also provide a solution to the vexing telco vs. OTT dilemma, if a suitable regulatory framework develops around that duality paradigm.”

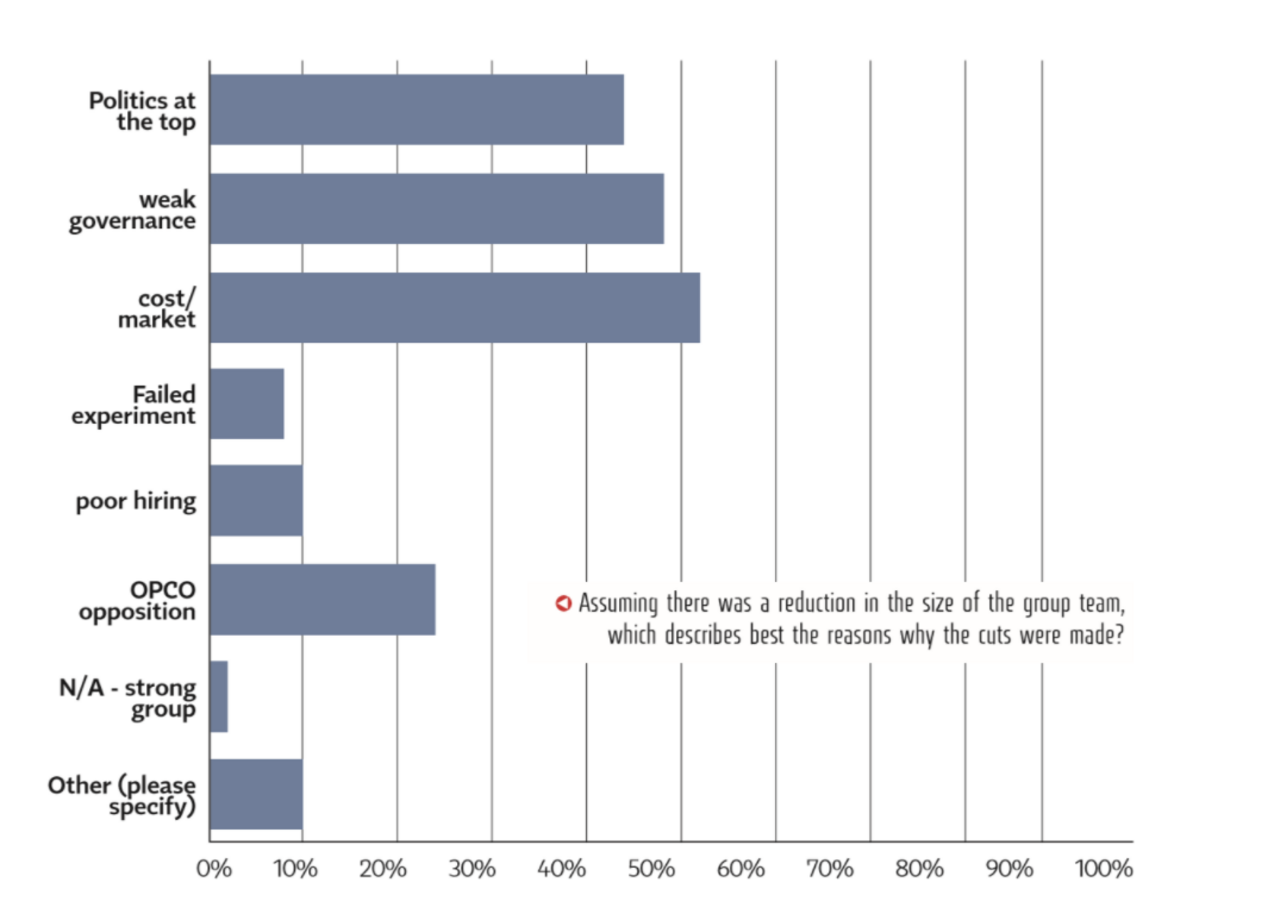

If telcos are to succeed in becoming the telco of the future, which operating model would support this? It is a known fact that the major regional telco operators have streamlined their group teams and moved to a less centralised model. 87.4% of respondents noted significant rounds of cuts to the group teams. In seeking to understand why, the three most popular answers were weak governance, politics at the top, and costs. A distant fourth was opposition from opcos to the notion of group interference. Only a small minority noted poor hiring decisions as the source of concern. The prevailing view was that the right people had been hired into a dysfunctional machine.

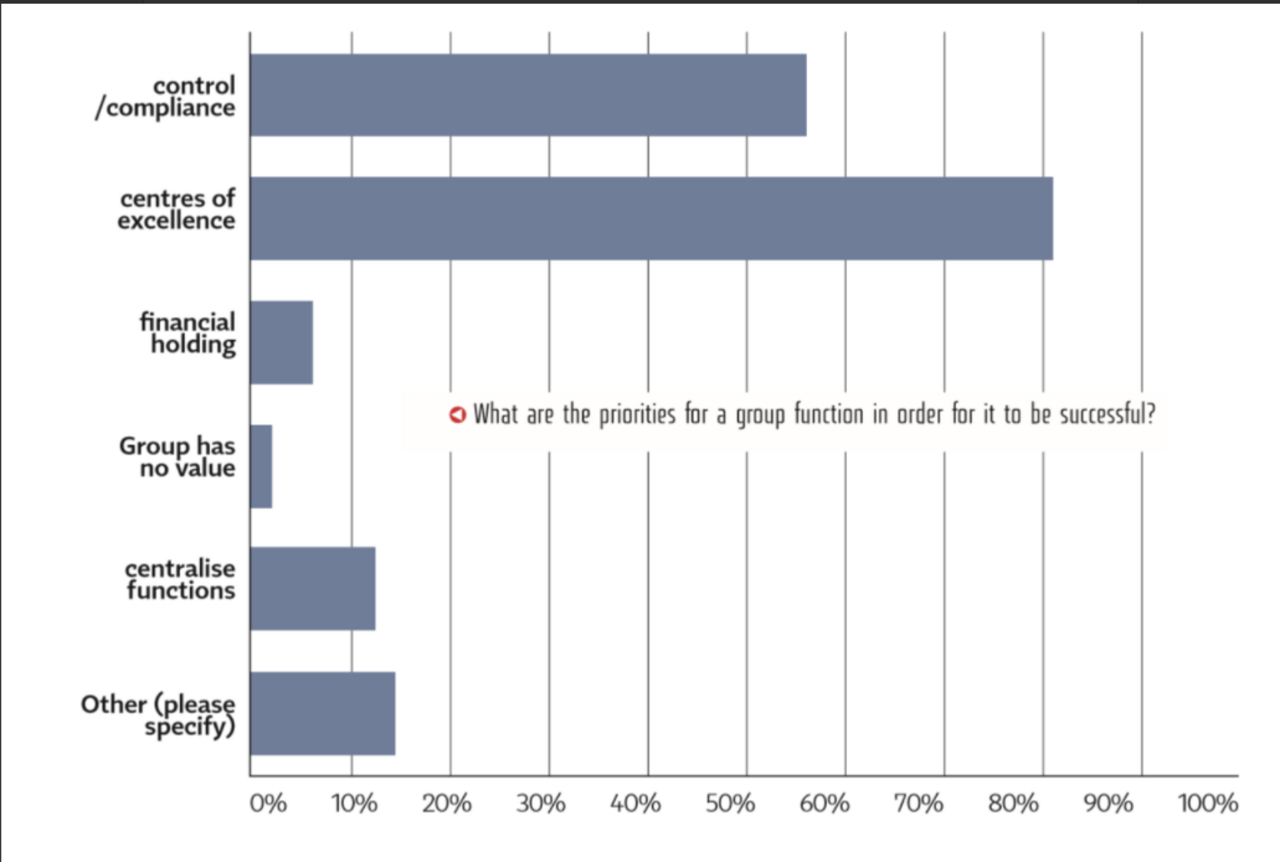

I would wish to look more closely at the comment on governance. If the group has no clear mandate or authority, what is the point of hiring large numbers of expensive executives to perform what amounts to an advisory role? I therefore sought to understand what the respondents felt the group should be doing, if indeed they felt it should exist at all. Despite what appears to be a move towards more of a financial holding company model in many cases, there is general support for the concept of a group, albeit with a very clear defined mandate. Only 7.4% of respondents felt that group should move to a financial holding company model or that it had no purpose. Equally, only 12.5% felt that most functions should be truly centralised with, for example, the country level CFO’s reporting directly to the group CFO.

Matthew Willsher, CEO Etisalat Nigeria summed up his expectations of a group team: “As a CEO of an opco, I particularly value the group when it is source of scale advantages, best practice and talented people. Scale advantages are the easiest to access; benefiting from best practice and talented people requires an open, trusting, and “bountiful” attitude from both the group centre and its opcos.”

Of the survey responses, the most popular responses were:

- Create centres of excellence, synergies between operations, global family etc (81.3%)

- Control functions; financial control, compliance, audit, risk, legal etc. (56.3%)

This begs the question of what we mean by centres of excellence and should it be for all functions? A major constraint is the political need to position a centre of excellence in the home country of the telco.

If the operator originates in the GCC, it is likely that the cost per head of a member of staff in a head office function will be significantly higher than in some of the subsidiary countries. This can present the scenario where it is actually cheaper in the lower cost markets to outsource some of the group functionality to the local branch of a consulting or professional services company rather than rely on group support.

If the operator is an incumbent in a cosy home market, it could follow that it has not been forced by competition to become excellent but merely slightly better than a wounded competitor. This is not to criticise. Sports teams can only beat the opponent they are up against and typically only truly raise their game when a strong opponent puts them to the test. Which operator is ready to identify that the actual centre of excellence in a particular function is in of the subsidiary countries and is ready to base the centre of excellence there? The other challenge is that when the portfolio comprises a number of operations at different points in their journey and in markets which often bear no relation to each other, is there any true value in a centre of excellence? Perhaps the synergies simply do not exist?

Perhaps there is merit in a group function, which performs a control function with a small PMO and strategy team looking for genuine pockets of excellence. A small co-ordination team might exist at group level but only to manage or encourage those true centres of excellence to share their knowledge. One commenter observed (anonymously) that “operators still think like franchises . Internet or web based companies think global first and iterate many times”. While the regulatory environment may contribute to this, it is also the case that operators perhaps try too hard to be local. Perhaps a strong global brand with global values as demonstrated by Google, Apple, Amazon and the like can work? If the operator is an incumbent, however, this is not as easy to achieve as the brand feels less global. Perhaps over time people will forget that Ooredoo is Qatar Telecom, STC is Saudi Telecom but we are not there yet!

“What about Emirates Airlines?” I hear you cry. As they land in multiple countries, they naturally connect with customers all around the world. This, backed up with heavy investment in marketing has led to Emirates becoming global. Telcos can only really achieve this if they diversify their business offering, as demonstrated by Telus, BT and others in offering non-core services on a global basis. This provides additional revenue streams and raises brand awareness in markets where they do not hold a mobile licence. This would seem a logical route to go and there is no reason why the regional telcos cannot explore this approach.

As the English proverb states: necessity is the mother of invention. For the first time in living memory, the region’s telco sector is facing genuine threats to its dominance. It needs to reinvent itself in order to thrive in the future. It is, according to the data collected, however, in an enviable position to grow from an already strong position. Although the industry faces a period of sustained challenge, I retain great faith in the leadership of the major operators and their ability to build the telco sector of the future.

Source: http://www.commsmea.com/17202-building-the-telco-of-the-future-a-2020-vision/1/