How has working from home/remote work impacted the Chief People Office/CHRO role in the PE sector?

Kathleen Dunton, Managing Partner, Boyden Germany and EMEA Practice Group Leader:

COVID-19 has accelerated remote work practices to an incredible degree. In the pre-lock down period, companies were most often unwilling to consider this option. If we consolidate the feedback from Boyden clients, we see that a vast majority of their employees would like to keep the possibility of working from home; companies will not be able to go back on this option. People like to have the freedom to choose how and where they work; more conservative organizations will have difficulties retaining and recruiting their top talents if they demonstrate that they are inflexible in this.

At the same time, CHROs are telling us that efficiency and productivity is suffering when it comes to brainstorming, defining a road map or reinventing new models. As Private Equity companies are under tight deadlines to perform, they need to carefully consider workforce capabilities and the capacity needed in order to deliver on their business plans. Knowing that Human Capital is one, if not the single most important asset a company has, they will need to take three variables into account – employee motivation, impact on operations and the financial results.

In future, the role of the CHRO / Chief People officer will be even more critical for defining the company culture and in driving the HR road map to meet value creation objectives. COVID-19 has increased the sense of urgency and the need to have modern, business oriented HR people. The HR function is facing a number of new challenges: they need to be creative to increase workforce engagement and commitment, to revisit company policies, define new onboarding processes, implement new tools while at the same time embracing the absolute necessity of diversity.

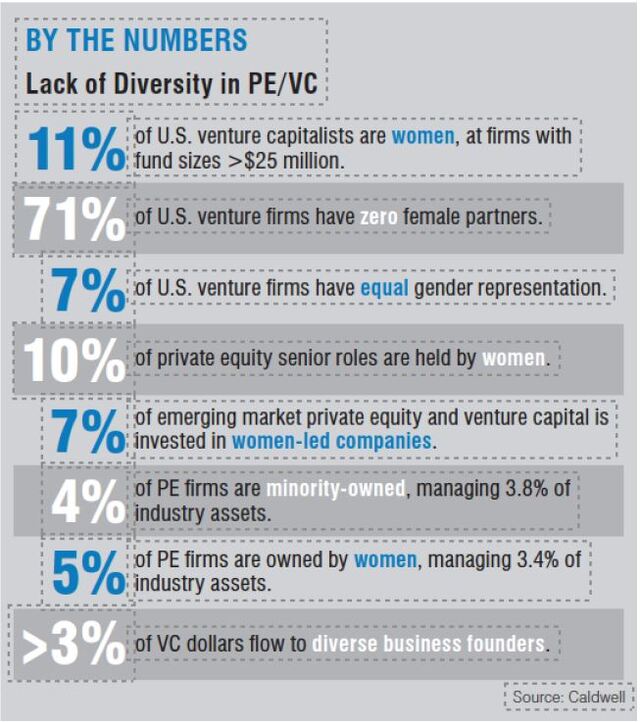

Research shows that organizations with diverse management teams have EBIT margins that are nearly 10 percentage points higher than those with below-average levels of diversity. Firms that take the lead on diversity initiatives can create a virtuous cycle that allows them to attract strong talent, nurture innovation, and lay the foundation for sustained growth.

The CHRO / Chief People Officer position requires a more modern and strategic approach to support the CEO in his/her plans, develop leaders, and create a culture that can make or break a company’s ability to meet aggressive performance targets.