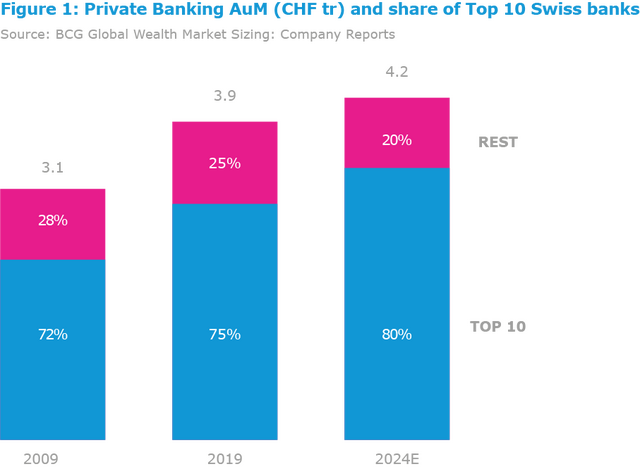

Global Wealth Management Industry Forecast

The wealth management industry has been resilient over the past decades despite the multiple crises, such as 9/11 and the 2008 crash, with global wealth almost tripling to $226 trillion from $80 trillion in 2000. Last year alone saw an increase of almost 10% from 2018 levels.

With the novel coronavirus, wealth is expected to contract in the coming months and the future will depend on the recovery trajectory. Boston Consulting Group identified three outcomes of this recovery in its recent report titled “Global Wealth 2020: The Future of Wealth Management - A CEO Agenda”1:

- Best scenario: growth rebounds quickly and wealth is expected to increase to $282 trillion in 2024

- Slow growth: wealth falls to US$215 trillion in 2020 and grows to US$265 trillion in 2024

- Worst scenario: wealth falls to US$210 trillion in 2020 and grows to US$243 trillion in 2024

Asia (excluding Japan) and Latin America are expected to continue to create new wealth faster than developed countries during this time and women's wealth will increase faster than men's.

BCG suggests that given the challenges that wealth managers will face over the next two decades due to Covid-19, as well as consequences from changing client needs and expectations of a new demographic of clients; companies will need to adapt their business models, product and service offerings to better serve clients. These include developing more-personalized value propositions, enhancing ESG and impact-investment offerings, investing in digital and data, and designing state-of-the-art technology platforms.

COVID-19: New Opportunities

Even before the pandemic, the Wealth Management industry was troubled by slow growth, commodification, digital disruption, and eroding margins. According to a recent Simon-Kucher research2, average AuM fees have declined from 1.01% in 2015 to 0.74% in 2019, due to the fact that wealth managers have not really been able to recapture the high profit margins they experienced before the 2008 crisis. Nevertheless, the biggest global wealth managers started the new decade in a strong position, driven by a buoyant market, positive client inflows and a generally improved profitability and cost-income ratio. Although the Covid-19 crisis is expected to reverse this trend, with depressed markets reducing the overall asset levels of the rich, there is a general confidence that private wealth management will navigate better through this recession compared to other divisions of banking.

When markets slumped in March as the spread of coronavirus gathered pace, wealth managers’ trading volumes soared as wealthy clients reshuffled their portfolios, bumping first-quarter profits at the world’s biggest wealth managers UBS and Credit Suisse, demonstrating the resilience of wealth management during crisis. The question now is how to sustain profits as market volatility and trading volumes subside. Many wealth managers have been focusing on finding investment opportunities outside of public markets, with increased activity in this segment recorded in the last six months, and efforts by banks and wealth managers to build dedicated teams to manage these investments. Opportunities include investing in distressed assets and lending more to businesses in need of cash, with private equity becoming a focal point especially in the fields of healthcare and technology.