Boyden Report Series

Volatility Is the Baseline: GCC CXOs’ 2026 Survey

GCC executives in 2026 are navigating intense geopolitical and operational pressures with cautious optimism, while facing critical leadership capability demands and a significant gap in succession readiness.

Introduction

The GCC's business leadership community operates in one of the most complex environments in the world. Geopolitical tension, cost pressure, and rapid market shifts have forced executives to make consequential decisions with incomplete information and to do so at speed.

In May 2026, Boyden MENA surveyed senior executives across the GCC to understand how leadership teams are responding. The results reveal a region that is resilient by necessity, cautious by instinct, and increasingly exposed in ways that demand urgent attention—particularly around the readiness of the next generation of leaders.

A Region Under Pressure

Geopolitics are at the centre of the C-suite agenda. 88% of respondents say geopolitical developments are influencing their business decisions—either significantly (46%) or moderately (42%). Just 13% say the impact has been minimal.

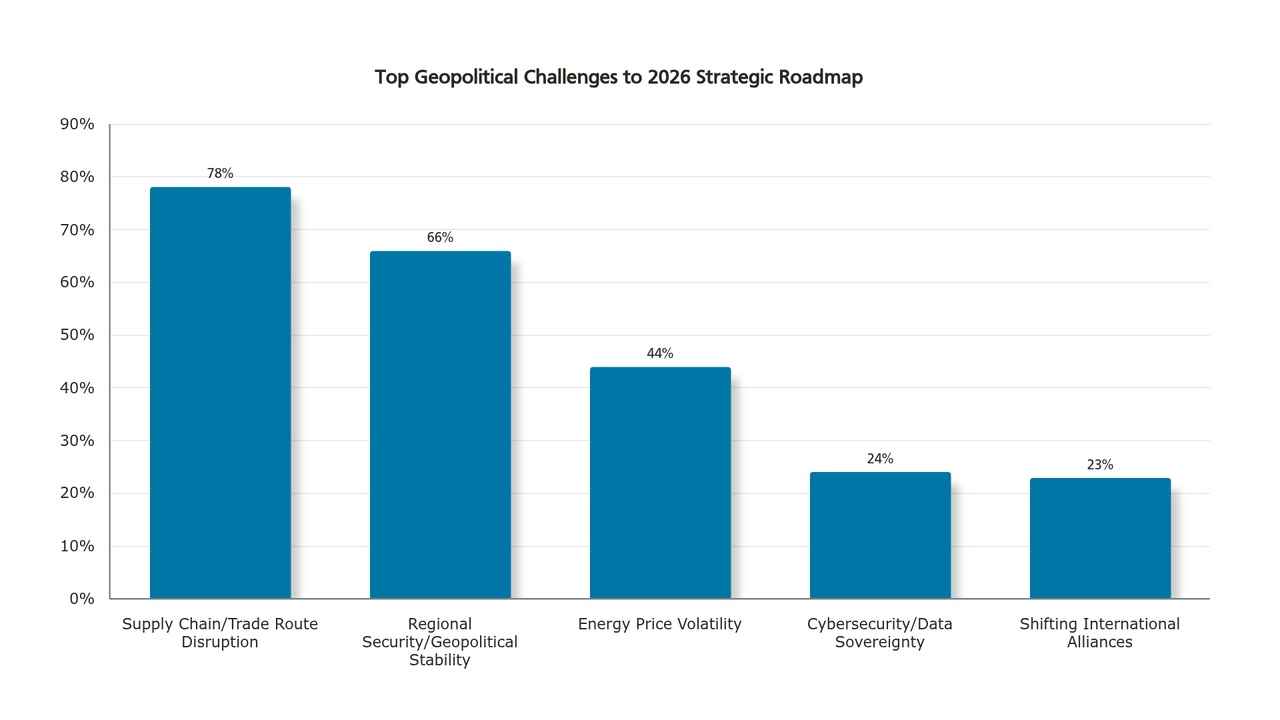

When asked about the greatest challenges to their 2026 strategic roadmap, executives pointed overwhelmingly to operational disruption:

- 78% cited supply chain and trade route disruptions (including in the Red Sea and Strait of Hormuz)

- 66% flagged regional security and geopolitical stability as a major concern

- 44% cited energy price volatility

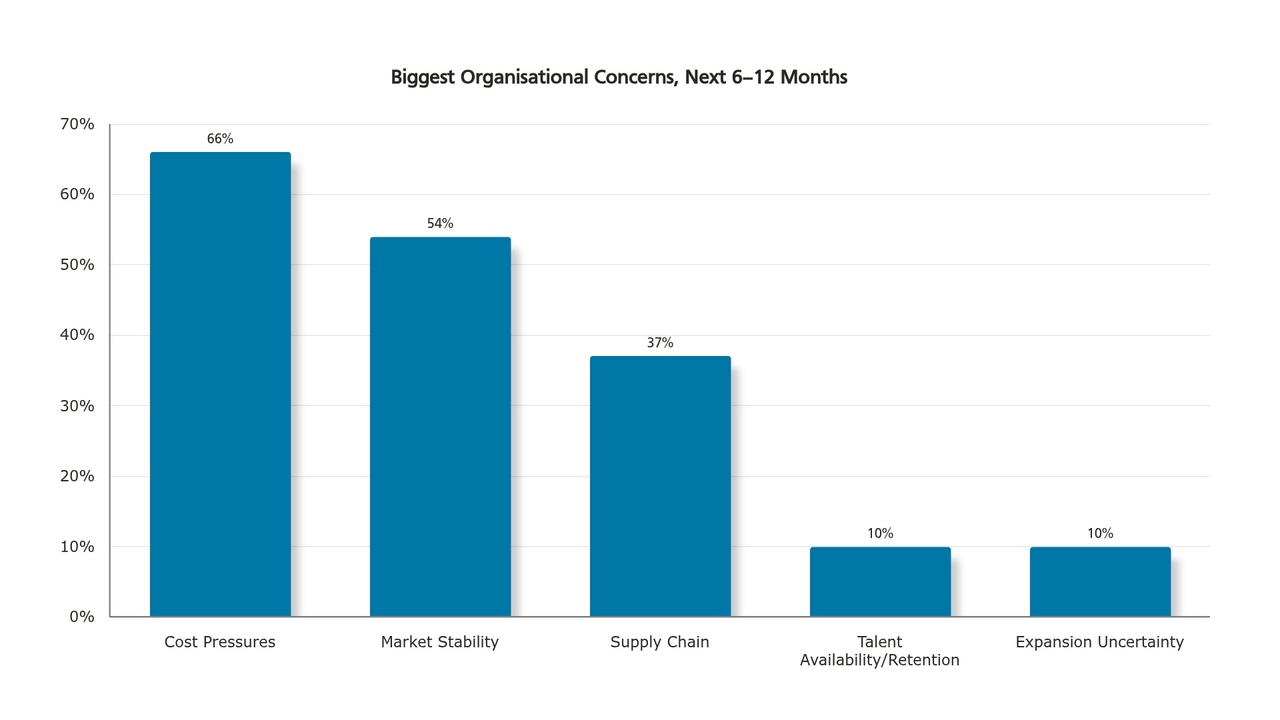

The cascading effect is visible in the biggest concerns executives identified for the near future: cost pressures, market stability, and supply chain.

Together, these findings point to an environment where margin compression and operational disruption—not growth—are the dominant preoccupations.

"The challenge over the next twelve months will be running agile, lean, and flexible organisations to withstand margin pressures until meaningful growth returns.”

— Magdy El Zein, Managing Partner, MENA

The Outlook — Cautious Optimism, Unevenly Held

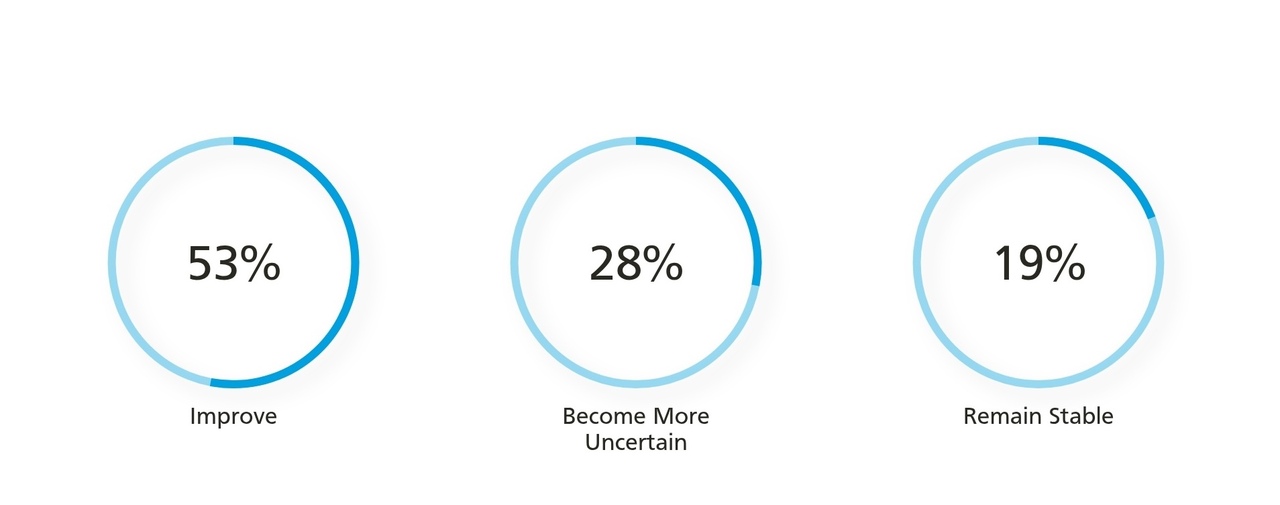

Despite the headwinds, executives retain a degree of forward confidence but it is far from uniform.

53% expect the regional business environment to improve over the next 12 months. Yet 28% anticipate greater uncertainty, and 19% expect conditions to remain flat. That means nearly half of the executive community does not expect meaningful improvement.

The divergence matters. In open responses, the dominant theme is unmistakable: geopolitical resolution will determine the trajectory. References to the Strait of Hormuz, regional conflict, and the need for political stabilisation appear repeatedly. One respondent summarised the prevailing sentiment: "The challenge of geopolitics should reach an end, no one benefits from escalation."

Several respondents with a Saudi Arabia focus offered a more optimistic view, pointing to Vision 2030 momentum and government-led private sector enablement. A minority of forward-looking voices pointed to AI investment and non-oil sector growth as structural tailwinds.

The implication for leadership teams is the need to stay flexible: managing current volatility while preserving options for moving decisively when conditions improve.

What Leaders Need Now

The survey asked executives to identify the most critical leadership competency for their organisations at this moment. The result was striking in its evenness.

Four capabilities were selected by virtually equal proportions of respondents:

- Strategic Growth & New Market Entry – 24%

- Digital Transformation & AI Integration – 24%

- Financial Restructuring / Efficient Capital Allocation – 24%

- Crisis Management & Resilience – 23%

The near-perfect distribution is itself a finding. In most markets at most times, one or two competencies dominate. The fact that these four register equally suggests that GCC organisations are not in a single strategic mode—executives are being asked to do everything simultaneously.

This places extraordinary demands on leadership teams. Executives are expected to pursue transformation and growth while simultaneously managing financial discipline and crisis response.

It reinforces the case for building deeper, multi-dimensional leadership benches—organisations cannot rely on a single leader to cover all four imperatives.

“This parity of focus signals a profound shift in corporate urgency—GCC executives are elevating crisis management and financial restructuring to the same level as strategic growth to navigate immediate volatility while building for the future, with leadership attention firmly fixed on what comes next.”

— Nessrine Salah, Managing Partner, MENA

The Succession Planning Gap — A Risk Hiding in Plain Sight

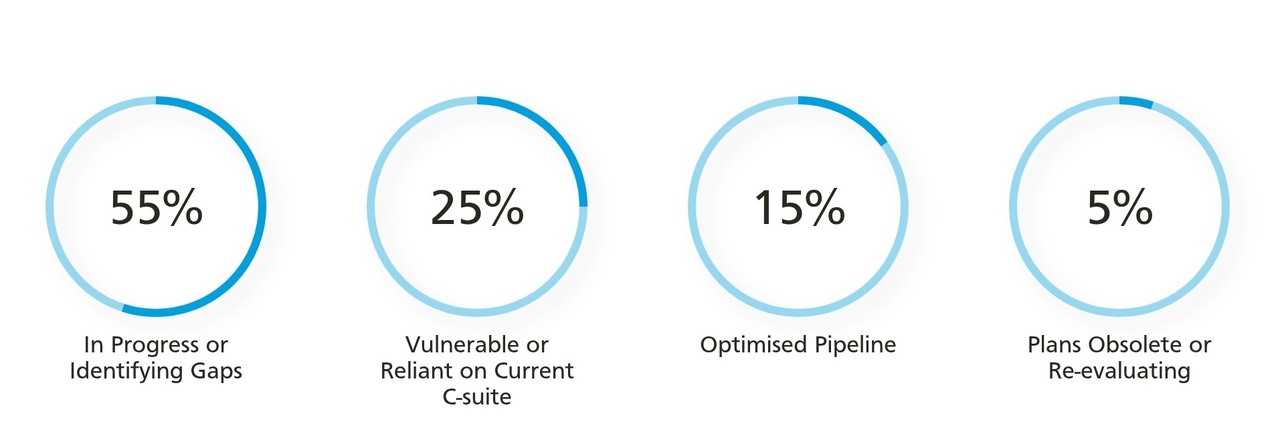

This is the finding that deserves the most urgent attention—85% of GCC organisations surveyed cannot confidently say they are succession-ready.

When asked to characterise their organisation's executive succession and bench strength, they painted a stark picture of structural vulnerability:

- Only 15% of organisations have an optimised succession pipeline ready for 2026/27

- 54% are still identifying gaps in their future leadership requirements

- 25% describe themselves as vulnerable, relying heavily on the current C-suite with limited immediate succession depth

- 5% say current market shifts have made their previous succession plans obsolete

The context makes this more acute. The GCC has historically operated on a model of expatriate-led, externally-recruited executive talent, but that model is now under strain. 51% of respondents say their perspective on senior talent mobility has become more cautious, compared to 25% who are more open and 24% who report no change.

Meanwhile, hiring is being tightened:

- 52% of organisations have slowed hiring or become more selective

- 27% have implemented a hiring freeze

- Just 4% are actively increasing hiring in key areas

Organisations that know their internal succession depth is insufficient are reducing their external hiring pipeline. The combination could be dangerous, particularly in a region characterised by geopolitical uncertainty and high leadership mobility.

“Relying on a stretched executive team in a region defined by rapid transformation and high talent mobility leaves organisations highly vulnerable; true operational resilience requires proactively de-risking leadership gaps by building deep, structured internal succession pipelines before vacancies arise.”

— Gabrielle Robinson, Managing Partner, MENA

The Talent Strategy Reset

Organisations are in the midst of a fundamental recalibration of how they approach executive talent—and not all of them have a coherent plan for what comes next.

The instinct to slow hiring is understandable. Cost pressures are real, uncertainty is high, and fiscal discipline is warranted. But executives who reduce external hiring without simultaneously investing in internal leadership development are compounding the succession risk identified above.

The more constructive response is a deliberate shift in talent strategy: from external acquisition to internal development; from headcount growth to increasing capabilities; from reactive hiring to proactive succession planning.

“It's understandable that organisations become more cautious in periods like these. What concerns me is when the response stops at slowing recruitment. The leadership challenges don't disappear; they simply shift elsewhere in the system. Critical roles still need successors, teams still need developing, and future capabilities still need to be built. In my experience, waiting is rarely a talent strategy. Using this period well requires resilience, informed judgement and a more deliberate approach to leadership decisions. For many organisations, this can become an opportunity to take stock of their leadership pipeline, strengthen succession plans and invest more intentionally in the capabilities that will matter most for the future.”

— Katia Pina, Partner, Leadership Consulting, Portugal

The organisations best positioned for the next 12-24 months will be those that used this period of constrained hiring to strengthen their internal leadership pipeline. When the environment improves, they will be ready to move.

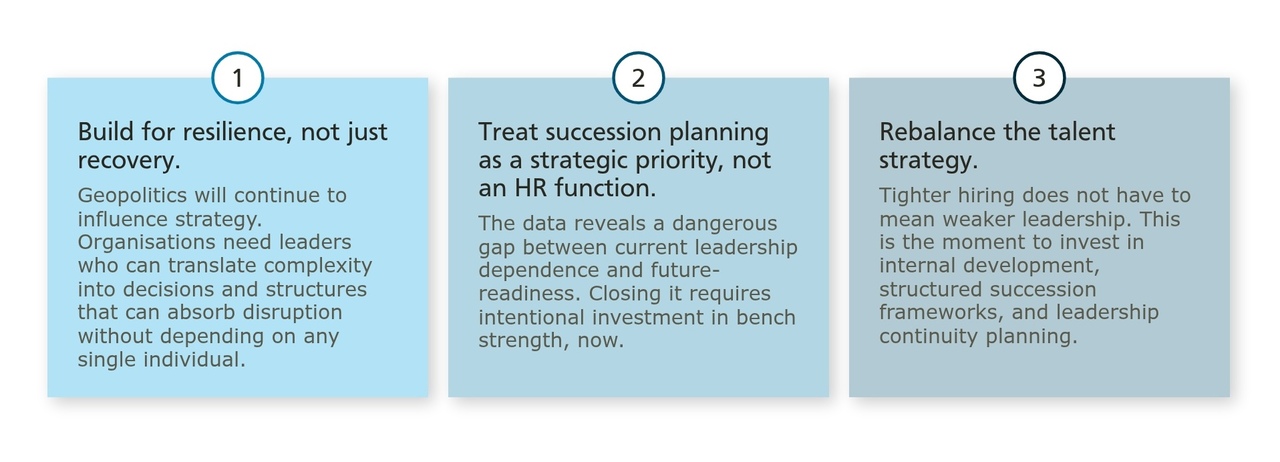

What This Means for GCC Leadership Teams

The GCC executive community enters the second half of 2026 in a position of informed vigilance. The direction of travel is broadly positive, but the path is uncertain and the risks are real.

Three imperatives stand out from the data:

The executives who lead their organisations through this period will be asked to anticipate what comes next and thoroughly prepare their teams to respond to it.

Methodology: This report is based on a survey conducted by Boyden MENA between May 6–19, 2026. GCC-based business leaders and executives were invited to participate in a 14-question survey exploring leadership, succession planning, talent, organizational priorities, and business outlook.

For organizations seeking to discuss their leadership strategy, Boyden MENA combines global expertise and regional insight to identify, evaluate, and place leaders who can navigate local complexities and drive long-term success.